Inversión

Soluciones holísticas de administración patrimonial creadas para satisfacer sus necesidades financieras.

Descubra el poder de su patrimonio

Estrategia personalizada

No hay una única solución para todo.

Por qué invertir con nosotros

En International Personal Bank U.S., hemos diseñado nuestros servicios de inversión en función de sus necesidades, permitiéndole trabajar estrechamente con uno de nuestros ejecutivos financieros en lugar de administrar sus inversiones por su cuenta.

Soluciones personalizadas

Ofrecemos una amplia gama de productos y servicios bancarios y de inversión para ayudarlo a crear una solución personalizada para usted. International Personal Bank U.S. le permite traducir lo más importante en una estrategia financiera detallada.

Guía de inversión profesional

Su ejecutivo financiero personal forma parte de un equipo con acceso a otros especialistas, incluyendo mercados de capitales, inversiones alternativas e inversiones internacionales, entre otros.

Con el respaldado de la solidez y los recursos de Citi, International Personal Bank U.S. empodera a los clientes de todo el mundo a trabajar para lograr sus objetivos financieros para ayudarles a disfrutar de los beneficios de la administración patrimonial basada en los Estados Unidos.

Sea usted un cliente que invierte por primera vez o un cliente actual, nuestro distintivo proceso de inversión está diseñado para ayudarle a desarrollar e implementar su estrategia financiera.

Determinar o validar su perfil de inversión

¿Cuáles son sus objetivos a largo y corto plazo?

¿Cuáles son sus necesidades de liquidez?

¿Cuál es su nivel de tolerancia al riesgo?

¿Cuál es su experiencia en inversiones y cuánto conoce los productos?

Nota: Esta inversión no se limita a los componentes indicados arriba

Revisar su distribución de activos

Analizar su cartera usando las perspectivas de inversión de Citi

Desarrollar o rebalancear su cartera personalizada

Revisar su cartera a su solicitud

Proceso de inversión adaptable de Citi

El proceso de inversión adaptable de Citi combina planificación a largo plazo con oportunidades y opiniones sobre el mercado a corto plazo alineadas con sus objetivos.

Fundamentado en principios establecidos a través de investigación académica, nuestro proceso adaptable hace uso de:

Un conjunto de oportunidades globales compuesto por diferentes tipos de inversión en todas las geografías

Estudios de historia de marcas financieras durante muchas décadas

Valoraciones actuales y estimaciones de rendimientos futuros

Medidas de los riesgos más relevantes para los inversores

El proceso de inversión adaptable asigna distribuciones estratégicas en función de:

Perfil de inversión individual

Diferentes grados de tolerancia al riesgo

Apetito de riesgo a la baja

Los integrantes de nuestro equipo dedicado trabajan juntos para su éxito

Mediante conversaciones directas con usted, un equipo multilingüe experimentado le ayuda a identificar sus objetivos financieros y lo apoya en la selección de una combinación personalizada de productos y servicios diseñados para ayudarle a trabajar para lograr sus objetivos y necesidades financieras particulares.

1 Disponible para clientes Citigold® Private Client International.

2 Análisis propio proporcionado por Citi Private Bank y otras entidades de Citi.

Manteniendo en perspectiva las condiciones cambiantes del mercado, las circunstancias financieras y sus metas de largo plazo, nuestro equipo dedicado de ejecutivos financieros identificará sus objetivos únicos para desarrollar su estrategia de inversión.

Cómo entender su nivel de tolerancia al riesgo de inversión

- Crear una estrategia financiera personalizada requiere la consideración de los riesgos financieros.

- Existe una ventaja comparativa entre el riesgo asociado con una inversión y su rendimiento esperado con el paso del tiempo.

- La tolerancia al riesgo se define como la sensibilidad de un cliente a la variabilidad de los rendimientos en su cuenta durante un plazo de un año, la disposición a absorber las pérdidas potenciales y la aceptación de poder liquidar las inversiones en forma oportuna o a un precio determinado.

- Cada inversor tiene una actitud distinta frente al riesgo y comprender esto es fundamental para encontrar inversiones que puedan ser correctas para usted.

- En función de una entrevista con su Ejecutivo Financiero, se establecerá su perfil de inversión en el momento de la apertura de cuenta, tomando en consideración su nivel de tolerancia al riesgo, las necesidades de liquidez, los objetivos de inversión, el plazo de inversión, los conocimientos y experiencia, y otros factores.

Tipo de niveles de tolerancia al riesgo

CONSERVADOR | ||

|---|---|---|

CONSERVADOR | Los inversores que esperan no experimentar más que pequeñas pérdidas de cartera en un período continuo de un año y generalmente solo están dispuestos a comprar inversiones que tienen un precio frecuente y tienen una alta certeza de poder vender rápidamente (menos de una semana), aunque el inversor puede, en ocasiones, comprar inversiones individuales que conlleven un mayor riesgo. | |

MODERADO | ||

MODERADO | Los inversores que esperan experimentar pérdidas de cartera no más que moderadas durante un período continuo de un año al intentar mejorar el rendimiento a más largo plazo y generalmente están dispuestos a comprar inversiones que tienen un precio frecuente y tienen una alta certeza de poder vender rápidamente (menos de una semana) en mercados estables, aunque el inversor a veces puede comprar inversiones individuales que conllevan un mayor riesgo y son menos líquidas. | |

AGRESIVO | ||

AGRESIVO | Inversores que están preparados para aceptar mayores pérdidas de cartera durante un período continuo de un año mientras intentan mejorar el rendimiento a más largo plazo y están dispuestos a comprar inversiones o celebrar contratos que pueden ser difíciles de vender o cerrar en un corto período de tiempo o que tienen una realización incierta valor en cualquier momento dado. | |

MUY AGRESIVO | ||

MUY AGRESIVO | Los inversores que están preparados para poner en riesgo toda su cartera durante un período de un año, y que incluso se les puede exigir que proporcionen capital adicional para compensar las pérdidas de la cartera más allá del monto inicialmente invertido, generalmente están dispuestos a comprar inversiones o celebrar contratos que pueden ser difícil de vender o cerrar durante un período prolongado o tener un valor de realización incierto en un momento dado. | |

¿Cómo transformamos su perfil de inversión, incluidos los objetivos de inversión y la tolerancia al riesgo en su estrategia financiera?

En International Personal Bank U.S., le ofrecemos mucho más que soluciones bancarias. Ofrecemos acceso a las percepciones y al liderazgo de Citi para ayudarlo a tomar las decisiones más informadas todos los días.

Opiniones sobre inversiones

Citi Perspectivas es una publicación bimensual destinada a brindarle la perspectiva económica de Citi, cubriendo los problemas más apremiantes que afectan su cartera. Esta publicación presenta:

- Datos analíticos: nuestras mejores ideas sobre los mercados financieros mundiales con foco en los mercados locales. Vea una muestra de Citi Perspectivas aquí

- Comentarios exclusivos: contiene comentarios del equipo de inversiones de IPB U.S., siguiendo los lineamientos de los principales analistas de investigación y estrategas de Citi

- Traducciones multilingües: disponibles en múltiples idiomas: inglés, español, portugués, ruso y chino

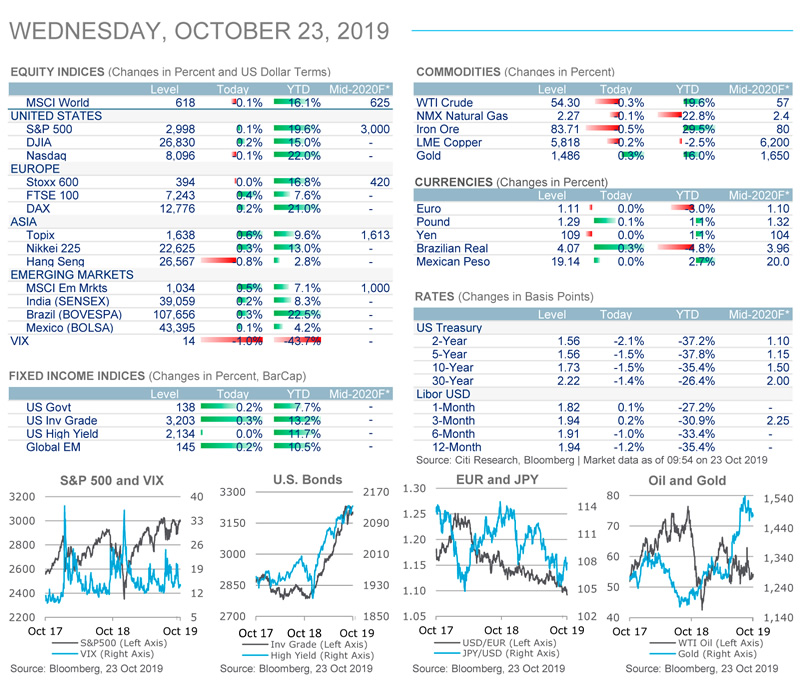

Actualización diaria del mercado

The Market Today le brinda información diaria de los mercados financieros, desde niveles de los índices y pronósticos de Citi hasta las noticias que mueven a los mercados todos los días.

Datos sobre los mercados

Acciones, renta fija, monedas y más

Que hay que saber esta mañana

Un resumen ejecutivo de las condiciones de mercado

Citi Global Perspectives and Solutions

Citi Global Perspectives & Solutions (Citi GPS) está diseñado para ayudarle a atravesar los desafíos más exigentes de la economía mundial, identificar temas y tendencias futuras y prosperar en un mundo interconectado y en constante cambio.

Citi GPS accede los mejores elementos de la conversación global de Citi y recopila perspectivas de los analistas de investigación y una amplia gama de profesionales sénior de la firma.

Tecnología en acción

La era digital producirá más conmoción que las revoluciones tecnológicas anteriores lo que generará alteraciones en la forma en que vivimos y trabajamos.

Obtenga Más Información sobre Tecnología en Acción

Innovaciones disruptivas VI

Los conceptos de vanguardia en los sectores nos ayudan a identificar productos nuevos que podrían desestabilizar el mercado.

Obtenga Más Información sobre innovaciones disruptivas

Migración y la economía

Una perspectiva detallada y equilibrada sobre el efecto de la inmigración en las economías avanzadas.

Obtenga Más Información sobre migración y la economíaACCIONES

- ¿Está buscando crecimiento del capital?

- ¿Se siente cómodo con las fluctuaciones diarias en el valor?

RENTA FIJA

- ¿Está interesado en ingresos por intereses periódicos?

- ¿Está buscando estrategias de preservación de capital?

OPCIONES

- ¿Quiere generar ingresos adicionales de las inversiones en acciones?

- ¿Está buscando limitar el potencial de pérdida durante las crisis de los mercados de valores?

FONDOS MUTUOS

- ¿Prefiere trabajar con administradores de fondos profesionales?

- ¿Desea acceder a una canasta más amplia de valores que podría variar según el sector, la región, la clase de activos y el producto?

PRODUCTOS ESTRUCTURADOS

- ¿Está buscando un producto personalizado que viene con beneficios derivados?

- ¿Necesita que su capital esté protegido?

CUENTAS CON ASESORAMIENTO

- ¿Requiere múltiples niveles de servicio y asesoramiento?

- ¿Está buscando control continuo?

- ¿Está dispuesto a pagar un costo anual por administración profesional?

INVERSIONES ALTERNATIVAS1

- ¿Quiere complementar su cartera con productos alternativos además de sus acciones y bonos tradicionales?

- ¿Es su plazo de inversión lo suficientemente largo para estar en inversiones ilíquidas?

La diversificación y distribución de activos no garantiza ganancias ni protege contra pérdidas.

1Las inversiones alternativas incluyen fondos de cobertura, entre otros.

El rendimiento pasado no garantiza los resultados futuros. Los inversionistas deben

analizar y considerar detenidamente los posibles riesgos antes de invertir.

Todas las

inversiones conllevan un riesgo significativo, incluida la pérdida del capital. Para ver

los riesgos de inversión detallados, haga clic aquí.

Nuestro proceso de selección de productos

Sigue un enfoque riguroso para seleccionar productos personalizados para usted

Información importante que debe saber sobre nuestro negocio y nuestra relación con usted

Se nos requiere entregar dos documentos de divulgación importantes acerca de nuestro negocio y nuestra relación con usted:

- El Formulario de Resumen de relación con el cliente (Formulario CRS) es un breve resumen de los servicios de corretaje y asesoramiento que ofrecemos.

- La Declaración sobre la divulgación de la Norma del mayor beneficio (Regulation Best Interest Disclosure Statement) es una descripción más detallada de los servicios de corretaje que ofrecemos y de las obligaciones que tenemos conforme a la Norma del mayor beneficio (Reg BI) al momento de hacerle recomendaciones como sus corredores de bolsa.

Por favor, revise estos dos documentos importantes en línea a través de los enlaces que aparecen a continuación. Si prefiere copias impresas, comuníquese con su ejecutivo financiero o llámenos a los números de teléfono indicados.

Citi Personal Investments International:

Formulario CRS Citi Personal Investments International

Declaración sobre la divulgación de la Norma del mayor beneficio (Regulation Best Interest Disclosure Statement) Citi Personal Investments International

Teléfono: 1-877-836-9141 (sin cargo desde EE. UU.) o 1-210-677-3793 (Número TTY: 1-800-788-6775)

¿Tiene Preguntas? Contáctenos

Los productos y servicios de inversión son ofrecidos por Citi Personal Investments International ("CPII"), un negocio de Citigroup Inc., que ofrece títulos a través de Citigroup Global Markets Inc. ("CGMI"), miembro de FINRA y SIPC, asesor de inversiones y corredor/intermediario registrado ante la Comisión de Bolsa y Valores (SEC). Las cuentas de inversión son administradas por Pershing LLC., ("Pershing"), miembro de FINRA, NYSE y SIPC. Los productos y servicios de seguros se ofrecen a través de Citigroup Life Agency LLC ("CLA"). En California, CLA opera bajo el nombre Citigroup Life Insurance Agency, LLC (número de licencia 0G56746). Citibank N.A., CGMI y CLA son filiales bajo el control común de Citigroup Inc.

Por favor, haga clic aquí para acceder a divulgaciones importantes.